Another consideration: Income stacking and tax rates

As highlighted above, capital gains and dividends are eligible for tax rates that are typically lower than income tax rates. Moreover, there are multiple tax brackets for capital gains and the standard deduction applies to them as well. However, the calculations of ordinary income and capital gains are not separate; they are combined.

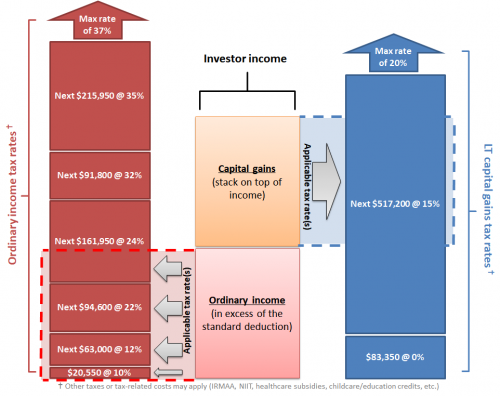

I find the most intuitive way to think about the combined calculation of income and capital gains taxes is to visualize them as being ‘stacked’ with ordinary income on bottom and capital gains on top. However, the ordinary income and capital gains are taxed according to their respective tax brackets and rates.

Ordinary income and LT capital gain stacking

Source: Aaron Brask Capital

Note: I did my best to reflect current tax rates and make this illustration to scale (as of 2022) but both the tax brackets and rates of taxation are subject to change.

Benefits of income ‘stacking’

There are two benefits worth highlighting here. First, stacking income with capital gains on top is beneficial for most tax payers due to the fact income tax rates are significantly higher than LT capital gains tax rates. If the stacking was reversed (with income tax on top of capital gains), then tax bills would generally be higher due to the higher marginal rates on ordinary income For example, last dollar of income depicted in this illustration is taxed at a 15% rate since it is a capital gain. If income were on top, this last dollar of income would be taxed at 35%.

The second benefit derives from the fact that LT capital gains taxation has a 0% tax bracket. This bracket exists above and beyond the standard deduction – which effectively functions like an initial 0% tax bracket itself. This additional 0% tax bracket for capital gains may allow for a significant amount of tax loss harvesting depending on one’s situation.

In retirement, we often want to make use of any spare capacity in lower tax brackets (see my article + video on income tax). However, there is another option: tax-gain harvesting. That’s right: gain harvesting. Some of you might be familiar with tax-loss harvesting but this is different. An example may be instructive.

Example: Let us assume Jane is single, 60 years old, has no ordinary income, and has a portfolio with unrealized capital gains. In this situation, she would be able to realize a significant amount of capital gains without paying any taxes. How is that?

Well, first she has her standard deduction ($12,550 in 2021). So there would be no tax on realized gains up to this amount. Then there is no tax on the capital gains in the first 0% tax bracket (up to $40,400 in 2021). So that means Jane could trigger as much as $52,950 ($12,550 + $40,400) in capital gains without paying a penny in capital gains taxes.

When these situations arise, it is almost always sensible to harvest the gains and re-establish the same or similar positions. This raises the cost basis of these positions and minimizes potential capital gains taxes paid later. However, you must be sure that all of the shares have gains. That is, it is possible that some holdings actually embed a loss even if the average price of that holding embeds a gain. If you sell a position that triggers a loss and then buy it back too quickly, you can violate the wash-sale rule.

Astute readers may have noticed I made two different recommendations for utilizing spare capacity in lower tax brackets: tax-gain harvesting (this article) and Roth conversions (my previous article). Prioritizing between or combining these strategies can be tricky. Complicating matters further are factors such as:

- Tax credits + eligibility for various subsidies (e.g., affordable care)

- IRMMA (investment-related monthly Medicare adjustments)

- NIIT (net investment income tax)

- Taxation of Social Security (watch out for the torpedo!)

As with income tax planning, I strongly advise utilizing a financial planner who uses financial planning software that is devoted to this purpose. I prefer Income Solver due to its superior calculation engine even if its interface and reports are less glamorous than other packages.

Unfortunately, I find many advisors opt for planning software packages that are easier to use and create more aesthetic (interactive) reports to show to their clients. Moreover, I believe it is also important for financial planners to augment software output to address areas the software does not (e.g., disclaiming and beneficiary strategies – see my video discussion of this topic on my videos page).