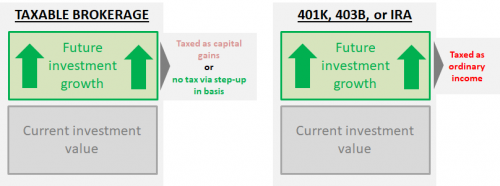

Some people claim it is better to pay taxes on money before it grows instead of paying a bigger tax bill (in absolute terms) after it grows. However, this logic is faulty. All else equal (tax rates, time horizon, and growth), paying tax at the outset or at the end results in the same exact amount of after-tax dollars being available at the end. The simple fact is that the tax rate applies multiplicatively and it does not matter what order you multiply numbers. If C is the original amount of the contribution, G is the investment growth, and T is the tax rate, then the amount of after-tax money at the end is the same:

Let’s follow what happens to $1 of retirement money when we contribute to a 401K that grows 10-fold to $10 while invested. The $1 becomes $10 via investment growth and then tax consumes $2.50 when it is ultimately distributed – leaving $7.50 to spend. Now let’s follow what would happen if we used a Roth 401K instead where we paid the tax upfront. In this case, we start with $0.75 in the Roth 401K and it grows 10-fold to $7.50 with no more taxes due. So the results are the same.

Truth be told, I brushed some details under the rug here; all else is not equal. For example, Roth accounts effectively allow for higher contributions. That is, we could have contributed one full dollar to the Roth if we had external cash on hand to pay the tax. Roth accounts also avoid required minimum distributions down the road. So that money may be able to enjoy the tax-shielding benefits longer than if they were forced out into taxable accounts.

On the flip side, taxes are typically lower during retirement. So it might make it more sensible to use traditional (non-Roth) retirement accounts. For more on these nuances, I went into significantly more detail here and here (warning: these articles are a bit more technical).